- Free Strategy Session: (847) 906-3460 Tap Here to Call Us

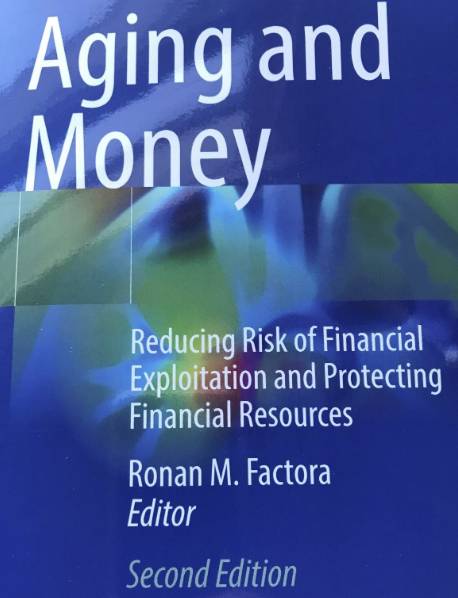

Aging and Money – Reducing Risk of Financial Exploitation and Protecting Financial Resources

With good reason, financial elder abuse has been characterized by some experts as “the crime of the 21st Century.”

– Broken Trust: Elders, Family and Finances. Metlife Study, March 2009

The second edition of Aging and Money was just released including a chapter that I co-wrote with Lisa Bleier of SIFMA, entitled Perspectives from Financial Institutions. This is a subject that I have been working on for years and this was a great opportunity to contribute to a book written for healthcare professionals.

The risk of financial exploitation of elders today is significant. In one case that haunts me, a financial advisor and his family took advantage of a customer as her dementia progressed. After befriending her, they isolated her from her family and abused a power of attorney they obtained to take unauthorized actions – including secretly maintaining complete control of the customer’s bank and brokerage accounts. They knew that the customer had an estate plan that provided for a family member to handle her affairs should she lose the capacity to do so. Yet, when the customer’s family, who lived far away, asked whether the customer had an estate plan, the financial advisor threatened to drag them through court. As a result, the truth did not come out for over six years, until after the customer died.

I also have an elderly family member whose declining cognition caused her to repeatedly fall victim to scams, including the Nigerian prince, even after she learned they were scams. She would continue to send money when she received phone calls. Nevertheless, I have elderly family members who refuse to take steps to protect themselves should their cognitive abilities decline. Many other lawyers, financial advisors, and law enforcement personnel have family members who they cannot convince to take precautions to protect themselves from elder financial exploitation.

Many of us are fiercely independent and want to remain that way until the very end. Many of us do not want to talk about money with family and friends. That is dangerous as we age. We need to connect with family, friends, or professionals who can step in when needed to protect us from financial predators.

Aging and Money is an important resource for healthcare practitioners to use in working with all patients to prepare for the cognitive decline that is common as we age. There were 52 million people over the age of 65 in 2018. Estimates are that over 5% of this group has been a victim of elder financial exploitation. This pool of victims will only grow as baby boomers age.

Many of us may not notice cognitive decline as we age. Others of us may refuse to recognize it. I have spoken to many family members of elders who have been swindled and remain unwilling to acknowledge that they need help. Despite my work on this important issue and my own family member being a victim, I have older family members who refuse to take steps to protect themselves from financial exploitation.

This subject gets media attention periodically when the victim is someone famous like Mickey Rooney or Brooke Astor. That might lead people to believe that this is a problem only for wealthy older people. That is not true. Many low-income and middle-income elders experience financial exploitation.

Healthcare professionals can be an important part of the effort to reduce elder financial exploitation. Clinicians are in a good position to assess and document the risk factors of patients. Medical records documenting the symptoms of dementia can be instrumental in the prosecution of the perpetrators of financial exploitation as well as in civil actions to recover the funds. By recovering funds or at least halting the exploitation, clinicians can play an important part in keeping an elderly patient from the extreme stress of losing a home, having to move to a nursing facility, or becoming a ward of the state.

The identification of risk factors along with advice about preventive steps can be an important part of healthcare for aging patients. This is a conversation that can start at a younger age when a person may be less concerned about losing their autonomy. People in their 40s and 50s may be more open to taking steps to protect themselves when contemplating financial exploitation that could take place years in the future.

In the chapter I wrote with Lisa Bleier, we address what financial institutions, including banks, brokerage firms, and investment advisers are doing to prevent elder financial exploitation. What clinicians call “mild cognitive impairment” affects a significant number of individuals over the age of 75 and can have a significant impact on an individual’s ability to make financial decisions. There are steps that financial institutions can take if they become aware that a person is at risk of financial exploitation. Organizations like SIFMA have created a great deal of educational material about elder financial exploitation. Our chapter identifies websites where clinicians can find these resources.

Abuse of Trust

A consistent theme in elder financial exploitation is that the perpetrator is usually someone who the elderly victim trusts: a family member, a close friend, a nursing home staffer, or a trusted financial advisor or accountant.

Clinicians are in a good position to not just identify when this exploitation has already happened, but to identify those at risk of falling victim in the future to such exploitation. Clinicians can encourage patients to establish a preventive system of checks and balances before cognition declines. For example, clinicians can ask patients if they have identified a trusted contact on brokerage accounts and if they have set up with their banks and investment firms to have statements sent to two unaffiliated persons – like a family member and an accountant.

Resources

Here are links to a few of the resources that SIFMA publishes showing what financial institutions can do to detect and prevent elder financial exploitation.

SIFMA Senior Investor Protection Initiative Client Protection Playbook, available at Toolkit Client Protection Playbook, Senior Investor Protection Toolkit.

The Red Flags of Financial Exploitation and Cognitive Decline, available here.

It was a pleasure to write Chapter 9 with Lisa Bleier of SIFMA. I appreciate the work that SIFMA is doing to overcome legal obstacles to financial personnel reporting suspected elder exploitation as well as SIFMA’s education and outreach work in this area. I look forward to future collaborations with Lisa. I also want to thank Dr. Ronan Factora and his colleagues for editing the book and Dr. Robert E. Roush for contacting me about the second edition and his tireless advocacy in this area. His enthusiasm and energy inspire me to do more.

You can learn more about the book here. Here is the table of contents.

This information is not legal advice and is provided for educational purposes only. This information does not create an attorney-client relationship. For legal advice, consult with a qualified attorney about your specific circumstances.